The second lever available to businesses seeking to transact to transform is capitalising on decarbonisation and other ESG goals as a value creation strategy. In fact, our Global Private Equity Responsible Investment Survey 2023 found value creation to be the top driver for ESG activity in private equity (PE).

Almost all investors are pushing for greater ESG accountability, and PwC’s latest research found investors want to know how a company’s sustainability plans square with its business model and its prospects for creating long-term value.

Linking M&A to decarbonisation and climate is a practical play in today’s global landscape. Notably, this goes beyond divesting carbon-intensive business lines—although, that’s one major strategy. Play 2 can also involve acquiring new capabilities (human and tech) and adopting new investment strategies and processes to pursue decarbonisation and other ESG goals.

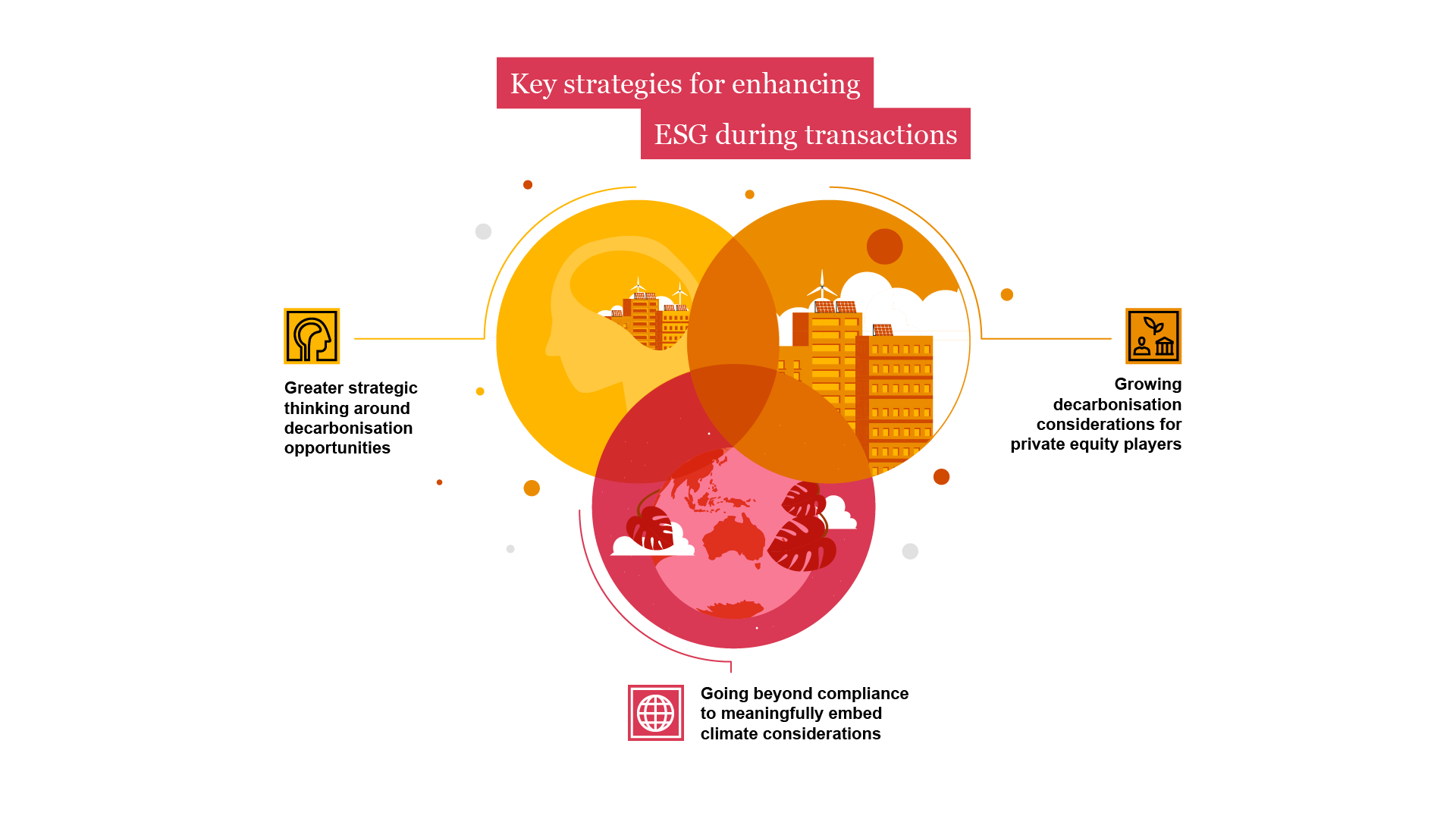

To generate real ESG uplift using M&A transactions consider these strategies:

With more fund-level decarbonisation commitments, and a clear commercial opportunity around carbon credits, funds are thinking more strategically about how to drive value in these areas. Carbon credits are only expected to increase in price. So, for some funds, the ability to directly generate and use carbon credits (and therefore accrete value in these companies) may also be a hedge for the fund’s overall performance, partially mitigating value deterioration in other heavier emitting, hard-to-abate portfolio companies.

Locally, we’ve seen this in action among forestry and/or land-heavy agricultural businesses with the characteristics to generate quality carbon credits (e.g. Morrison & Co’s acquisition of Pastoral Partners), or companies with project development expertise (e.g. KKR and Ontario Teachers’ Pension Plan investment in GreenCollar, and Adamantem Capital’s investment in Climate Friendly).

Overseas, we’ve seen the launch of a carbon credits investment company (Terra Natural Capital); transactions involving carbon and environmental commodity trading platforms (e.g. Blackstone’s acquisition of Xpansiv); and transactions in energy management (e.g. Blackstone and Vista Equity’s acquisition of Energy Exemplar from Riverside). We’re also seeing a broader focus on carbon emissions along the supply chain (i.e. Scope 3), including investments in electric vehicle freight for logistics, cold chain storage solutions, and sustainable packaging.

To date, global decarbonisation efforts have largely focused on energy transition and climate funds (think Brookfield and Blackstone), and often involving large-scale investments in renewable energy projects, carbon capture solutions, and transition from fossil fuels (e.g. Brookfield and Mike Cannon-Brookes’ attempted AGL takeover). However, there’s increasing recognition of the role that mid-market PE funds must play in tackling hard-to-abate sectors across all industries, beyond oil and gas.

Given their typically shorter investment horizons, some PE players are still weighing up whether to commit to firm decarbonisation targets. At the same time, others such as Adamantem Capital and Crescent Capital are establishing funds where all future investments are committed to accelerated net zero targets, in order to secure favourable funding. They are then using their influence to guide their portfolio companies on the net zero journey, helping to future-proof these companies.

Globally, there is momentum to standardise climate-related financial disclosures, and the Australian Government looks set to finalise its mandatory climate reporting regime. Therefore, the implementation of climate management frameworks is rapidly becoming a ‘must have’, and strategies for addressing climate change are no longer something that can be dismissed or postponed. This has far-reaching implications for every industry sector.

While Australia’s upcoming reporting rules will not directly apply to most private institutional investors (noting they will impact super funds), we are already seeing investors embrace climate-related analysis and reporting. In a transaction context, the global alignment on methodology is much more than a ‘tick a box’ exercise; it’s an opportunity to strategically and systematically embed climate considerations into due diligence, financial forecasts, asset allocation strategies, and mitigation plans at a whole-of-portfolio level.

The reporting landscape will continue to evolve. The Taskforce on Nature-related Financial Disclosures (TNFD) recommendations were released in September 2023, for example. Rather than view these changes as another compliance exercise, this is an opportunity for investors to get ahead of the curve on nature and biodiversity; already, we’re seeing a growing number of dedicated ‘natural capital’ funds in the EU and UK markets.

Checklist for dealmakers to go further, faster

Explore the need-to-know checklist for dealmakers to bring this play into action

Contact us