{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

At PwC, we are conscious of increasing community and stakeholder expectations upon businesses to build trust and provide transparency. As auditors, we maintain a long standing commitment to provide transparency around the quality of the external financial statement audits that we do for clients.

This scorecard provides a collective view of PwC Australia’s performance on audit quality – across a range of measures from sources both internal and external to our firm.

It details PwC’s internal inspection results for the year ended June 2022, and any restatements arising from those reviews. It also includes the most recent ASIC audit inspection results (June 2022, published October 2022). Our ultimate goal for our inspection results is that ASIC considers that we have obtained reasonable assurance in all audit areas.

One of the newer quality measures included in this scorecard pertains to the views of clients, captured through an annual feedback process using a defined set of audit quality variables. This process enables us to respond with targeted actions to enhance the client’s experience and our ability to provide a high quality audit. By sharing the feedback insights report with our client, we acknowledge their feedback and our commitment to act on it, promoting greater transparency in the relationship.

Taken together, the measures shared in this scorecard provide a holistic representation of PwC’s performance on audit quality against the appropriately high expectations set by the market, the regulator, our clients and the PwC global network.

We recognise that expectations of our firm and of the auditing profession around audit quality are increasing. The economic uncertainty of the past three years has intensified the need within our community to seek trust and confidence from independent sources. We understand that high quality audits are critical to helping build integrity and confidence in the capital markets to help protect investors and the choices they make.

PwC is committed to continuous improvement in its audit quality and respects the results of all reviews. Our quality improvement plan includes conducting a formal root cause analysis for each finding and creating actions to address them.

As part of our commitment to audit quality, at PwC we also draw upon the objective review of the PwC Australia Audit Quality Advisory Board (AQAB), which provides feedback and advice on how we can improve the quality of our audits. The executive summary of the third annual AQAB report back to PwC, including its recommendations for improvement and what we’ll be doing to execute on them, are contained in our 2022 PwC Australia Audit Transparency Report. As such, this scorecard should be read in the context of our current Audit Transparency Report.

Together, these documents represent the latest steps in our commitment to providing greater transparency about our audit business.

Download the FY22 ASIC PwC Audit inspection report (312 KB)

Download the FY22 ASIC Audit inspection report (470 KB)

"Economic uncertainty has intensified the need for trust and confidence from independent sources. High quality audits help build integrity and confidence in the capital markets."

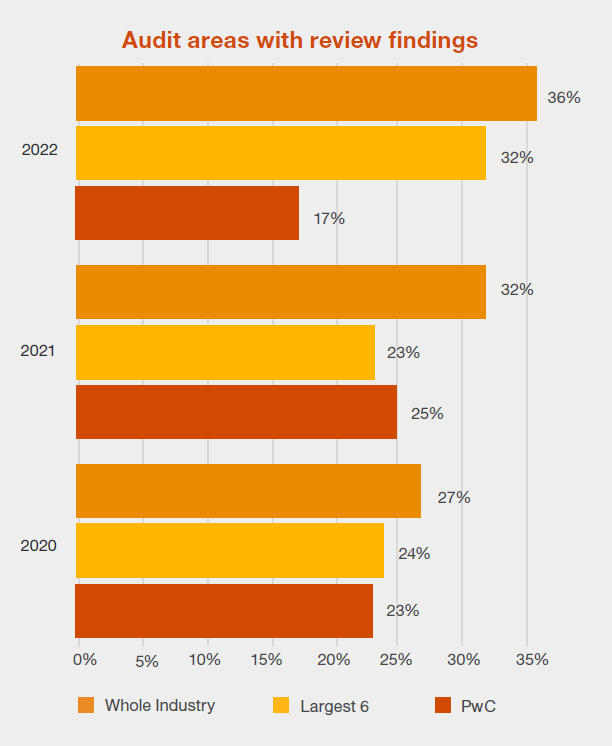

As part of its audit inspection programme, ASIC reviews a sample of audit files at each audit firm focusing on high risk areas in listed company audits. ASIC’s most recent audit inspection results (June 2022, issued October 2022) pertain to audits covering financial reports for years ended from 31 December 2020 to 31 December 2021. In its report, ASIC noted that many of these financial reports and audits would have occurred under COVID-19 conditions.

In ASIC’s report to PwC Australia in four of the 24 key audit areas reviewed across 8 PwC audits (17%), ASIC considered we did not obtain reasonable assurance that the financial report was free from material misstatement. This compares to 36% across the whole industry, and 32% at the six largest firms in Australia. For context, PwC Australia signed more than 7,100 audit opinions across approximately 1,800 clients during the review period.

We will undertake a root cause analysis of all the findings in ASIC’s report and build these learnings into our continuous improvement process. A full copy of ASIC’s audit inspection report for PwC Australia for the year ended 30 June 2022 is available on our website.

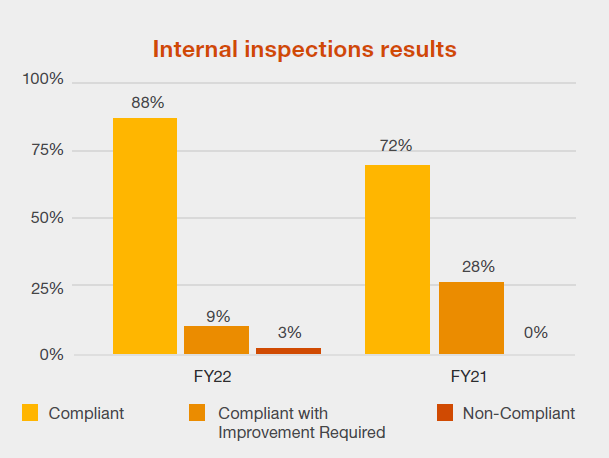

PwC Australia is subject to globally coordinated quality inspections because we are part of the PwC network. The inspections are coordinated by a global team and led by representatives from other PwC member firms, not Australian representatives. The findings are independently moderated by the network inspection team. Inspection outcomes are summarised by rating an overall audit file as “compliant” or “non-compliant” with PwC network standards, which are based on International Standards on Auditing (ISAs).

In 2022, 1 file out of 34 reviewed was rated non‑compliant with network standards. This compares to no file rated as non-compliant with network standards in 2021.

The identification of a finding in an ASIC or PwC Australia audit inspection means that a certain element of the audit, be it design, execution or documentation of audit testing has not, in the opinion of the reviewer, met the requirements of the relevant auditing standard. This does not, however, mean that the underlying financial statements to which the audit relates are materially misstated.

In 2022, when issues were identified in external or internal audit inspections of PwC audits of publicly listed companies, there were no cases where there was a resulting restatement.

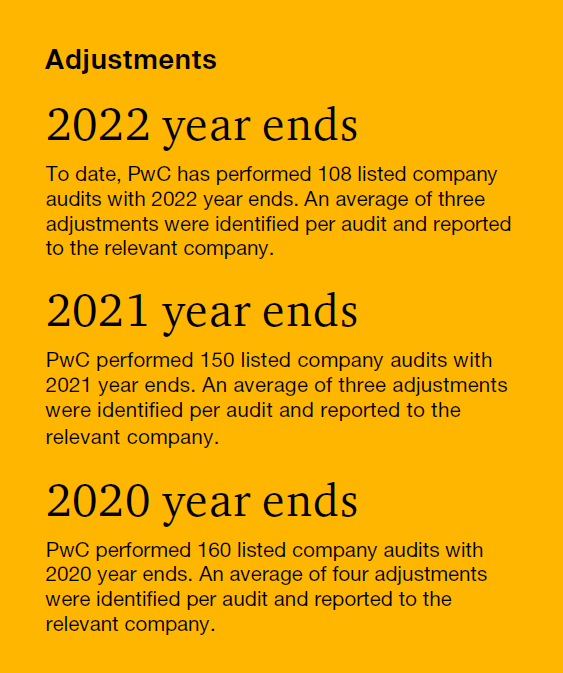

There are many cases where a company makes adjustments to its financial statements, or clarifies or enhances its disclosure, before they are published, as a result of the audit. While not always visible to the market, they are a tangible measure of a quality audit.

The identification and resolution of these matters requires sound risk assessment, deep technical knowledge and an ability to raise issues with management and the audit committee, sometimes in difficult situations.

In 2022, PwC audits of listed companies have identified to date, on average, three potential adjustments per audit, and ensured their appropriate treatment, prior to finalisation of the company’s financial statements.

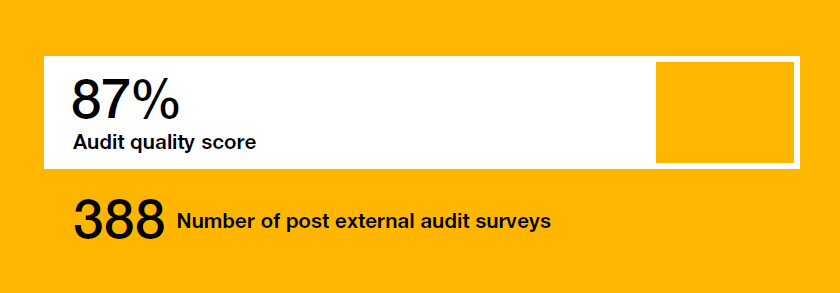

We use a defined set of audit quality variables to survey audit clients. These variables cover the depth of our team’s knowledge of the client’s business and industry, the differentiation of our technical expertise, the effectiveness of the tools and technology we use and the planning we undertake, as well as our mindset of respectful challenge.

This year from the post external audit surveys we obtained an audit quality score of 87%. This compares to the baseline score of 81% achieved in the inaugural year in which we conducted the survey. In addition to this, PwC people (independent of the audit engagement) conduct feedback conversations with key audit stakeholders.

This process enables us to respond with targeted actions to enhance the client’s future experience and our ability to provide a high quality audit. By sharing the feedback insights report with our client, we acknowledge their feedback and our commitment to act on it, promoting greater transparency in the relationship.

Independence is a fundamental part of audit quality. It ensures our objectivity.

Regulatory and professional standards limit the services auditors can perform for audit clients.

Collectively they seek to prevent the auditor being put in a position of auditing their own work, acting in a management capacity or as an advocate for the company. Audit committees of listed companies have responsibility to approve the company engaging their auditor for any services outside the audit.

At PwC Australia, we also understand community concern about auditor independence when a company they audit is also accessing a range of other services from their firm. We therefore support the Parliamentary Joint Committee on Corporations and Financial Services’ recommendation in 2020 for a standardised approach to disclosure of audit and non-audit services and greater clarity of the definitions of relevant categories.

We take independence and conflict risks seriously. Our annual PwC Australia Audit Transparency Report outlines our policies and systems that support our requirements to comply with all regulatory, professional and independence requirements related to financial interests in, and business and services relationships with our audit clients.

A number of stakeholders have raised questions that have suggested professional services firms operate unprofitable audit businesses as a “loss leader” to promote other services within the firm. In our experience, this view is without any basis of fact.

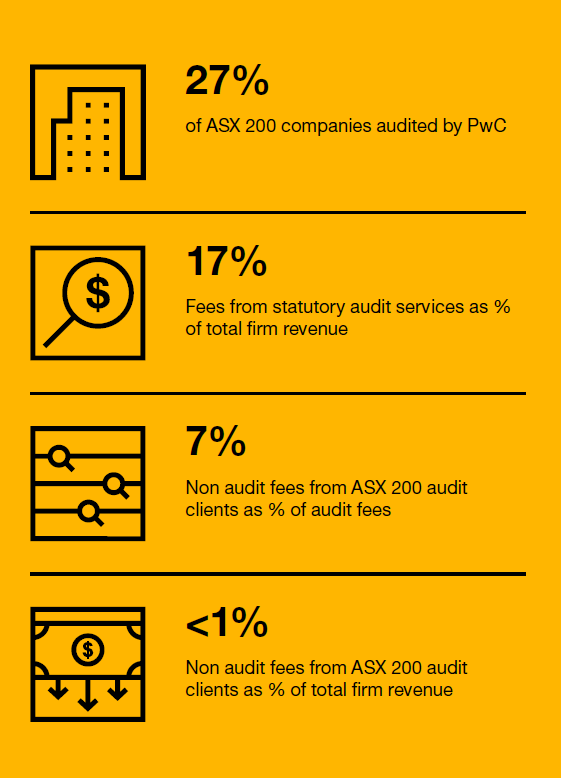

PwC Australia is proud to be the leading audit firm in Australia, auditing 27% of the ASX 200. In FY22 our total revenue relating to audits of financial statements was $503m representing 17% of total firm revenue. In FY21 it was $468m, representing 18% of total firm revenue.

The level of profitability across our Assurance, Consulting and Financial Advisory businesses is broadly equal. No audit partner is incentivised, evaluated or remunerated based on selling non‑audit services to their audit clients.

From time to time, when independence regulations allow, audit clients may choose PwC as the best option when a project needs external assistance. This work will be considered through our own internal independence and conflict processes when they arise before any work commences.

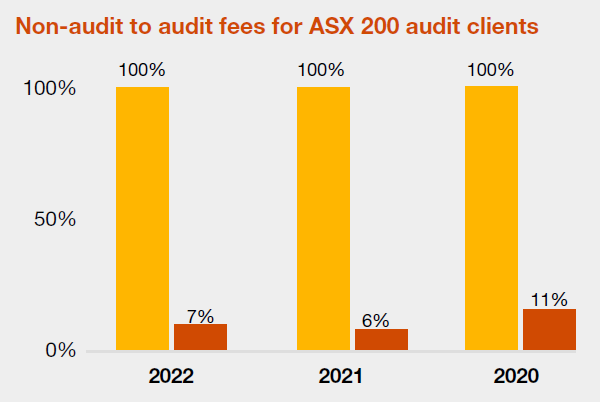

Notwithstanding, non-audit fees from ASX 200 audit clients have approximated 7% of total audit fees in FY22, representing less than 1% of total firm revenue.