{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

2022 AGM season: a return to normalcy

The 2022 AGM season - that is companies that held AGMs during 1 January 2022 to 30 December 2022 was marked by a return to the levels of strikes and no votes that we experienced prior to the COVID-impacted 2021 AGM season. While there were similar issues such as the application of discretion and the need to determine the ‘right’ outcomes that balanced all stakeholder needs, this AGM season was marked by fewer strikes and the lowest average no vote since 2017.

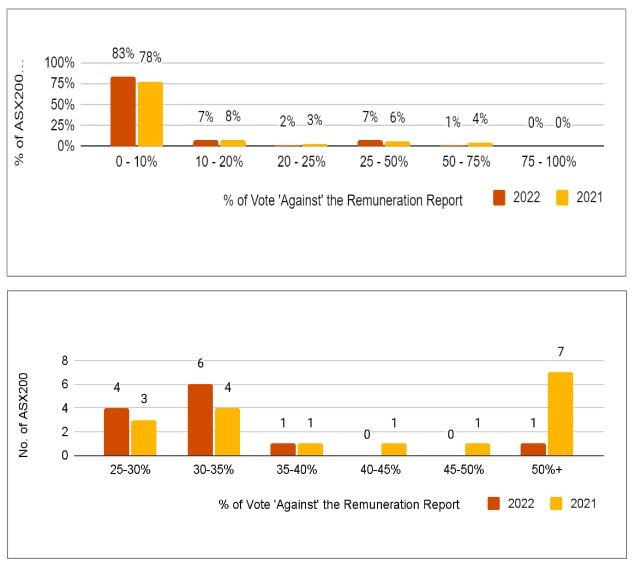

Twelve companies received a strike in the ASX 200 - that is a no vote of greater than 25% against their remuneration report. Approximately 8% of companies received a strike, down from 11% in 2021. It was a similar result whether we were looking at ASX 100 or ASX 200 companies. The average no vote was the lowest level since 2017 at 6.5%, driven partly by the far fewer extreme no votes (i.e. over 50%), particularly compared to last year. This year we saw only one company receive this as compared to seven in 2021.

Notwithstanding, four companies received a second strike, but all avoided the spill motion.

When we look at what is happening this season, it feels like a return to normalcy. But we're seeing new challenges arising. Inflationary pressure is placing pressure on remuneration as is the uncertain economic environment.

Continuing issues, although far fewer large no votes

2021 featured a number of strikes that reflected shareholder dissatisfaction with broader company performance or governance issues, but the strikes for 2022 were grounded in remuneration issues. That is, executive pay that appears to be excessive, whether that’s fixed pay or bonuses, insufficiently challenging performance metrics, retention awards, application of board discretion in favour of management and broader governance issues. The misalignment of views from shareholders and boards on pay for performance is a continuing debate with the board squarely in the seat of needing to not only answer the question of “what is fair”, but appropriately disclosing and articulating the framework and rationale behind that answer.

That is, there may be criticism of poor disclosure rather than what the actual decision is, and how it is disclosed and articulated externally.

Comparing the voting outcomes for 2022 to 2021, the first chart shows the distribution of voting outcomes. We saw a lot more companies in the 0 - 10% of votes against the remuneration report as compared to 2021. The second graph looks at just those companies that received a strike and is skewed somewhere between 25 - 35%, compared to above 40 - 50%. That also contributes to the low average no votes seen this year.

Historically, proxy advisors and shareholders have scrutinised and criticised the use of some non-financial metrics where it is used in the STI or LTI plans on the basis that they are seen to be part of an executive’s day job. In prior years this could be a key reason for the no vote. However, this doesn’t seem to have contributed to remuneration strikes this year, notwithstanding 39% of ASX 100 companies incorporate a non-financial measure in their LTI.

What the future holds: the big issues

While this year may feel like a return to normalcy, there are increasing pressures for boards to consider or to take action on remuneration to better attract and retain talent. These include inflationary pressures - which may ease towards the end of the year, greater job mobility and low unemployment rates. This could see companies thinking about the need to allocate one off grants of equity or retention of awards.

There's always going to be a need for boards to consider the quantum of pay increases and bonuses in line with performance and shareholder expectations and what's happening in the broader workforce. They also need to ensure their remuneration framework and targeting appropriately reflects desired performance outcomes, and the judicial use of discretion. We see four areas emerging:

Other trends we are observing include:

Deep Dive 1: ESG

ESG: The gap between pay and purpose in executive pay

Every client of ours is talking about ESG and how to reflect it in executive pay. Our first advice is to have an ESG strategy and policy before you put the ESG metrics in for executives. Some clients like a gateway or some form of ESG measure to ‘tick the box’, but don't have a well informed, coherent, comprehensive approach. It really needs to be that way around rather than ‘the tail wagging the dog’.

85% of the ASX 100 have some measure of ESG within the STI but only 9% in the LTI. The technical argument would be that ESG creates long term valuation - so why isn't it in the LTI? Some of that has to do with what are the targets or specific measures that fall under the umbrella of ESG. Even with the STI, if you've got a financial component of 70% you really only want four to six big measures to be effective. But we’re seeing 8 to 14 measures when you unpack it all. And in the end, some ESG and gender measures might only amount to 1 or 2% of the overall weighting of the incentive, which really diminishes the impact.

It's far more progressed in the FTSE 100, where we’re seeing more than half in the LTI. and a much more mature debate on the use of restricted stock within the UK market. In the US we're seeing some organisations rallying against ESG within the measures.

ESG metrics: what is a priority?

We have a number of ‘old’ measures of ESG such as employee engagement and customer satisfaction that fall under the S of ESG and we have new measures such as net zero climate emissions or change metrics. Many measures around environment, governance, risk management, compliance, sustainability might already be in place. If, for example, you have a gateway in your incentive plan for non-compliance or risk management, you've already got part of the G in the ESG. Some companies might be tempted to bundle the existing measures under an ESG umbrella without changing anything. But proxies and investors will see that through that, particularly if it's trying to be a gateway or look back based on existing measures. Investors are looking for something new and distinct.

LTI measures more often incorporate climate related metrics such as carbon transition, sustainability, and related penalties. These are seen in the use of discretion, or downwards discretion or negative multipliers for policy breaches. For example, at Santander, a deferred component of its senior management incentive scheme is dependent on achievement against performance of levels of green finance raised and facilitated through the bank’s loan portfolio and decarbonisation in its investment portfolio. Also Tesco introduced food waste reduction as a metric in its LTI scheme, supplemented by incentives with other ESG measures such as carbon reduction and leadership diversity. I advised a co-op group in the UK that not only used community donations for leftover food as part of a metric, it also used it as part of the EVP to be differentiated as an employer by applying some of its ESG metrics. We will have some research later on in the year that will be testing what value employees place on ESG measures and whether they help to attract and retain. Finally at Mars, 20% of the LTI is assessed on GHG emission targets and 20% on an externally monitored societal reputation metric.

Diversity: an emerging focus

Only 12 companies in the ASX 100 incorporated a D&I gateway or metric and they were exclusively gender related. These included individual behaviours, females in roles, number of women in leadership, female graduate hires. A progression against the scorecard of D&I actions is quite prevalent. There was one example of indigenous employees being hired as well.

We’re seeing both diversity and climate metric getting more traction in the financial services sector with new regulations and the need to explore non-financial metrics. We’re also seeing mining, resources and extractive clients have been talking about this for a decade or longer, particularly around non-financial metrics. But there are no instances of D&I metrics in the LTI. The prevailing thinking is that long term success is built up by achieving a number of short term achievements and we don't necessarily see that changing quickly due to the scepticism that non-financial measures are more easily achieved. Recent data has shown that non-financial measures pay out more than financial, but not significantly more, which means that companies generally do a good job in setting those targets.

The ongoing challenge will be with so many measures to put in incentive plans, which ones do you choose? Again, we're already seeing measures being worth 1% of the overall weighting. If the intention is to change behaviour, what impact will this actually have?

Deep Dive 2: Non-financial metrics in LTI

LTI metrics are changing

One of the debates in most boards would be around a number of non-financial metrics being seen as the day job for executives. The challenge is how to set stretch targets for them. Within financial services, we know that the requirements under CPS 511 have a significant portion of non-financial metrics which need to be chosen and included in the framework. Almost 40% of the ASX 100 incorporate some form of non-financial metrics in the LTI. As mentioned, none of the strikes that resulted during the year were influenced by non-financial metrics in the framework. Companies are doing a much better job disclosing and being transparent on their non-financial metrics and the increasing pressure to disclose targets particularly in STI retrospectively. This has been mitigated somewhat by the quality of disclosures in annual remuneration reports for the STI. Pressure to disclose targets prospectively and retrospectively will continue. Although there's still some hesitation, we are seeing a number of large organisations retrospectively disclose targets in STI. One of the sensitive issues around non-financial metrics is just what are they? For example a behavioural measure for your CEO may not be prudent or commercially appropriate to disclose as a non-financial metric, even retrospectively.

Evolution of LTI practice

Below are some case studies which demonstrate the evolution of LTI and non-financial metrics:

These examples show just how complex this area is becoming. We often get asked if we can make this more. But all of the debate around non-financial metrics, the number, the setting and disclosure all increase the complexity. The alternative is to give people a restricted share or large shareholding for the long term but unfortunately it’s not that simple in the short term.

Q&A

What suggestions, tips or tricks would you have for those that are contemplating ESG into an LTI to try and help keep that as simple as possible?

There is pressure to put ESG metrics in the LTI. The accumulation of ESG performance year on year drives long term performance. The challenge is setting the right targets. Old measures like customer and employee can more easily be included in the LTI. But there is a strong argument to put environmental type questions around carbon emission and net zero targets into the LTI. Because we rebase the matrix every year, we have to set a target for the subsequent three years every year. I would encourage a smaller number of measures in the STI before running too fast and putting it in the LTI.

LTI sits over multiple periods but ESG expectations from investors are changing year on year. What passed muster 12 months ago, may not going forward. Setting targets over three years can be challenging. With STI, we have the flexibility to change year on year and are not locked into something that isn’t quite right three years down the track.

Do you have an example of a listed organisation where the CEO has agreed not to take full STI award to recognise they are well paid, and to bring an equity lens into an organisation?

There have been examples where the board has exercised negative discretion because of 100% payout of an LTI, where the share price has reduced. Six or seven years ago, BHP had ongoing 100% vesting, but the share price had declined and they cut the LTI vesting because the total quantum was cut by 25%. That had more to do with the shareholder experience and alignment question, rather than being well paid.

In one particular board meeting we were looking at the CEOs package, in terms of fixed pay which was sitting below where that person could be on a market median basis. While not publicly disclosed, that individual requested that if there was to be any pay increase, for it to be allocated to the senior leadership team and below.

The relative increases have been skewed to the workforce rather than executive. We consistently see salary increases for executives lower than the overall workforce budget, which feels appropriate, particularly given the cost of living.

During COVID, we saw reductions in pay and short term incentives hit that senior population much more so than the broader population. Boards kept the equity lens in mind, as well as senior executives.

What do you think the appetite is for the regulation around limiting the number of board roles people can take on? Have we seen a change with proxy advisors influencing this area? What could it look like if it was regulated?

I don't think we will see prescriptive regulation around the number of board memberships. We are seeing higher scrutiny and that may lead to increased workload. It is almost self-selecting - do you have the ability to give the right time and energy? I'm not sure that we are going to see regulation that says you can only have x many board memberships. As we have seen regulatory action against directors of major casino operators, other companies might start to think if we were held to that standard, do we have the right balance of people including the depth of skills and time commitment?

When we looked at the FTSE 100 in the UK a while ago, the median number of directorships was three. I would be surprised if it was much different in Australia. Amongst ESG and time commitment of NEDs, proxies will spend more time looking at this but I haven't come across anything around specific regulations.

It is certainly something the nominations committees would need to consider as people come on. Often people will add something but take something away at the same time, or seek something when their term is up. It is interesting to see it coming up as an issue again, it has been some years since it has been discussed broadly.

We know that the number of directors with cyber and digital skills is relatively limited. Directors with cyber experience may need to ask themselves whether they have the right time to execute on those responsibilities. Further, keeping in mind diversity measures around culture and gender, there are similarly smaller pools of talent to draw from.

Even the skills that you need to be a Remuneration Committee Chair are different now than two or three years ago. It is becoming a tougher job, particularly as the remit of committees start to widen in terms of HR and succession, particularly in FS.

Proxy advisors are also playing a role in this. Some have developed a point system where if you get more than six points (1 point for a NED role, 2 points for a Chair, 1.5 for a Committee Chair) they will start to question it. In the listed space, just the reading requirements makes you realise having 5-6 board roles in any event is too much.

What is your view of the LTI being awarded in a stepped 3 year cash component, particularly where there are illiquid shares and inability to flex too much and where we got multi jurisdictional key management. We have got the same challenges of Europe versus the US, versus Australia in terms of tax. I’m aware that some of the top end of town are doing this but are you seeing any pushback from management?

We are working with a couple of clients with low free floats. On the cash component, with illiquid shares, it is difficult to sell the shares or pay the tax. I am an advocate for partially settling some of the equity in cash. I wouldn't phase that vesting over 1-3 years. But if it is a 3-4 year vesting, then a proportion is settled in cash and a proportion is released in equity, allowing tax to be paid. The other way to do that is to deliver the cash component on through forced net settlement rather than the choice of net settlement. There are a couple of techniques, particularly with the low free float. I advocate a three year LTI as a minimum and a STI with a deferred component. With these examples I am working on, 50% delivery or settlement of cash also applies to the STI deferred component, not just the LTI, instead of all equity, half delivered in cash half delivered in released equity. The question then is at what point are the shares sufficiently liquid to not deliver in cash. In my opinion getting the volume up to that 30 or 40% becomes less of an argument. Globally, that is certainly the case for countries where it is difficult to administer. It is normal to deliver a phantom equity type arrangement that mirrors the current equity plan, but delivered in cash rather than equity.

On the step three cash component, proxy advisors look at the differentiation between the STI and the LTI. You might say, long term incentives are building to long term value, the same could be said for short term incentives. If it is less than three years, that might need to be explained or result in a cross on their checklist.

In terms of the global jurisdictions, an organisation might have a phantom plan, but it has to be managed at an individual level. They might want one overarching plan for everyone to the extent possible. But from an administrative complexity perspective sometimes it falls on the executive to manage those impacts.