Energy Regulation: Developing a value-driven regulatory response capability in your organisation

As Australia forges ahead in its energy transition journey, the scale, pace and volume of regulatory reforms in the National Electricity Market is substantial. There is an increasing expectation for organisations to be able to anticipate and respond more quickly to changes than ever before. However, it is also increasingly important for regulatory functions in utilities to be more strategic and value-driven to go beyond ‘just compliance’. In a market where changing consumer and sustainability demands are putting pressure on utilities to make fundamental shifts in what and how they generate, transmit and distribute power; being proactive, strategic and commercial in their response to regulatory reforms will be crucial and this requires different capabilities and plans.

The energy transition is driving significant regulatory activity - more disruptive, high volume and fast paced

The energy transition is well underway. In Australia, like other similar global markets, this is changing the energy system from a largely centralised model relying on power plants using conventional energy sources to a more decentralised model where variable renewable energy (VRE) sources. VRE is already generating ~ 28% of the nation’s electricity. This shift is driving a wave of regulatory reforms intended to help the industry accelerate and adapt to the change.

The push to meet net zero targets, the national conversation around coal, the conundrum of energy affordability, reliability and security, and the constant regulatory efforts to adapt to the evolving way we ‘power’ our nation are all defining the national electricity market right now. The latest energy reforms are complex in scale, wider in stakeholder impact.

There are some marked characteristics of the ecosystem at play here.

While the wave of regulatory reforms in NEM are critical to the success of the transition, recent rule changes like the Power of Choice, Five-Minute Settlement (5MS), and Global Settlement have shown us how these transformative reforms result in multi-million dollar implementation programs for the market participants. The implementation of 5MS alone has hit the industry with “an estimated $200-$300M in the competitive sector alone” according to the Australian Energy Council. While four years after implementing Power of Choice, there are still challenges to deliver the intended customer benefits due to challenges in scaling the smart meter penetration.

The regulatory changes and requirements will intensify over the coming years with more disruptive reforms already in the pipeline including the Post 2025 electricity market design and cross-industry reforms such as the Consumer Data Rights (CDR). Scrutiny on compliance and spend is growing and as consumer advocacy bodies play a more proactive role in shaping the industry.

The traditional approach where regulatory reforms equate to minimum viable compliance will need to evolve if businesses are to succeed in tackling the volume and pace of regulatory changes while generating value for their business stakeholders. There is a pressing need to reimagine what regulations mean to the sector participants and whether they intend to get more bang for the bucks, above and beyond compliance.

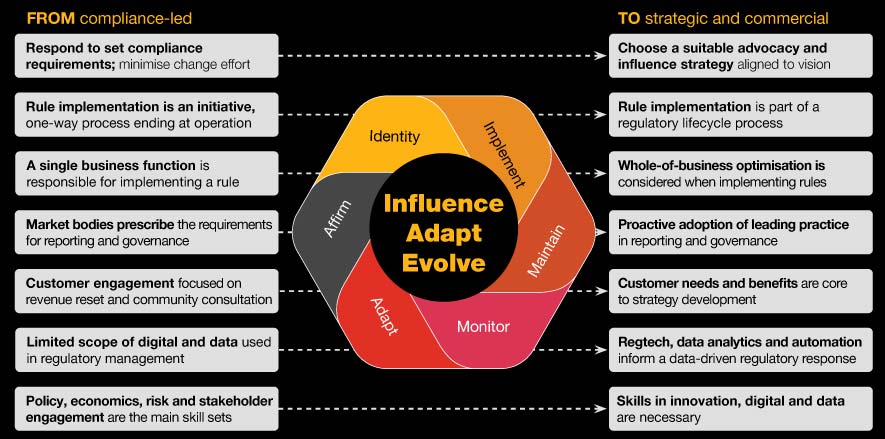

An effective regulatory capability can drive the organisation’s role in energy transition - by helping influence, adapt and evolve with change.

The regulatory function is at the centre of tackling energy transition - it can influence, adapt and evolve utilities’ transition agenda, and in doing so move away from being a largely compliance-led function to focussing more on strategic direction, customer outcomes and commercial returns to shareholders.

There is a need to reimagine the regulatory response and management capabilities beyond stakeholder engagements and impact assessments. These new capabilities must include the ability to influence reform outcomes at industry level, to derive the hidden costs and opportunities for customers and communities early on, and to confidently correlate the reform objectives to the organisation’s strategic directions and measures. This will help the organisations to plan ahead and rethink rule changes to their own benefit, thus giving them the confidence to take some timely no-regret actions.

For energy players looking to navigate the regulatory reforms in coming years, these are our observations on the shifts currently happening in the sector.

1. They proactively influence the direction of the reforms with a clear strategy in mind

| From ... | To ... |

| Response to regulatory changes is based on risk assessment, compliance requirements and focussed on minimising change effort | Vision, customer and innovation strategy drives positioning in the market and the adoption of appropriate regulatory advocacy approach |

|

|

|

|

|

|

|

|

2. They have relentless focus on customer outcomes when adapting to regulatory changes

| From ... | To ... |

| Preparing for regulatory submission or implementing a regulatory change is often a major one-off initiative relying on people and their past experience | Regulatory reforms are managed as portfolio of changes, data-driven, informed and measured by ongoing customer engagement activities |

|

|

|

|

|

|

3. They continually evolve their capabilities and measure success

| From ... | To ... |

| Regulatory requirements have been traditionally specific to the nature of the utilities’ role within the industry value chain | Regulatory requirements are increasingly becoming more holistic across customer, safety and economic benefits, regardless the type of utility or the role in the energy value chain |

|

|

|

|

|

|

A value-driven regulatory response capability can and will deliver sustainable business outcomes.

The changes to the regulatory function are based on our observations on the shifts happening around the world and the movements within the energy ecosystem in Australia. Some of the recent reforms and the way the industry tackled it also gives us evidence of what benefits are embedded in moving to a strategic, value-driven approach to regulatory responses, instead of a minimum viable compliance focus. Points in case are the Power of Choice and 5MS, where the costs ran into hundreds of millions and the benefits still arguably undetermined.

Some of the capability changes will not be easy as they require not just a change in the scope of what a typical regulatory function does, but also change in ways of working, acquisition of new skills and knowledge, as well as the need for further collaboration across a myriad of internal and external stakeholders such as customers, regulators, government, partners, and with the wider industry participants.

As organisations gradually shift their thinking and capabilities as discussed above, they will start delivering sustainable outcomes.

1. Cost efficiency. A clear plan and vision ahead of time and a predetermined, but agile approach to tackling a rule change will help utilities bring internal and external stakeholders together ahead of time, have a clear voice in the market and shape the program well in advance. When costs of compliance are viewed beyond the regulatory function and risk management, but in terms of long-term return and justified business advantages, investments and their benefits will follow. There will be:

- Reduced remediation and compliance costs

- Reduced regret rework

- Avoided fines and penalty of compliance gaps

- Faster and stakeholder-aligned response

2. Customer and stakeholder confidence. The strategic commercial lens to regulatory response advocates the involvement of customers and relevant external stakeholders early in the process. The consultations must be more than an information session and more a requirements gathering and accountability process. This will lead to:

- Increased transparency

- Increased customer trust

- Increased confidence from the broader stakeholders including regulators, partners, and peers

3. Organisation resilience. Being focussed on future-proofing the organisation and its outcomes, and taking a whole-of-business approach to internal and external stakeholder engagement and program set up will ensure there is:

- Increased agility in the businesses to apply changes

- Organisation-wide collaboration and accountability for change

- Faster decision making environment

- Enhanced innovation outcomes

4. Effective energy transition. It might not be an exaggeration to say every rule change in the next 2-3 years is focussed in some form or another in driving change towards decarbonisation. The energy transition is here and taking a strategic view of opportunities of growth and innovation from these reforms will ensure organisations are able to take:

- Well-justified investment decisions

- Balanced view on risk and opportunity

- Consideration on whole-of-system impact

As we open up more discussions on value-driven regulatory responses, there are some critical questions to ask as the energy sector navigates the big reforms ahead and as it tackles the most important problem in this generation.

Do we merely comply or move further to influence the regulatory outcomes?

Will we be compliance-led or lay a strategic and commercial lens to what we can do with a rule change?

Will regulations just be seen as a threat and inconvenience, or will we seek new innovation opportunities?

Will we be guided by the regulators or play a proactive role to drive the energy transition?

Contact us

Follow PwC Australia