{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

Hero image above and attribution here

Cashless payments were already on the rise, and the COVID-19 pandemic has only accelerated that trend.

Evolution of payments systems and a structural ecosystem revolution is reshaping the industry.

To navigate the future, financial institutions need to be aware of six emerging themes.

The financial services industry is in the midst of a significant transformation, accelerated by the COVID-19 pandemic. Electronic payments are at the epicentre of this change, as consumers become increasingly cashless, and the industry’s role in fostering inclusion becomes a significant priority.

A new report in PwC’s 2025 & Beyond series, Navigating the payments matrix: Charting a course amid evolution and revolution examines the payments industry and the key factors influencing it. How the industry responds to macrotrends will define how successful it is in the coming years and its impact on society overall.

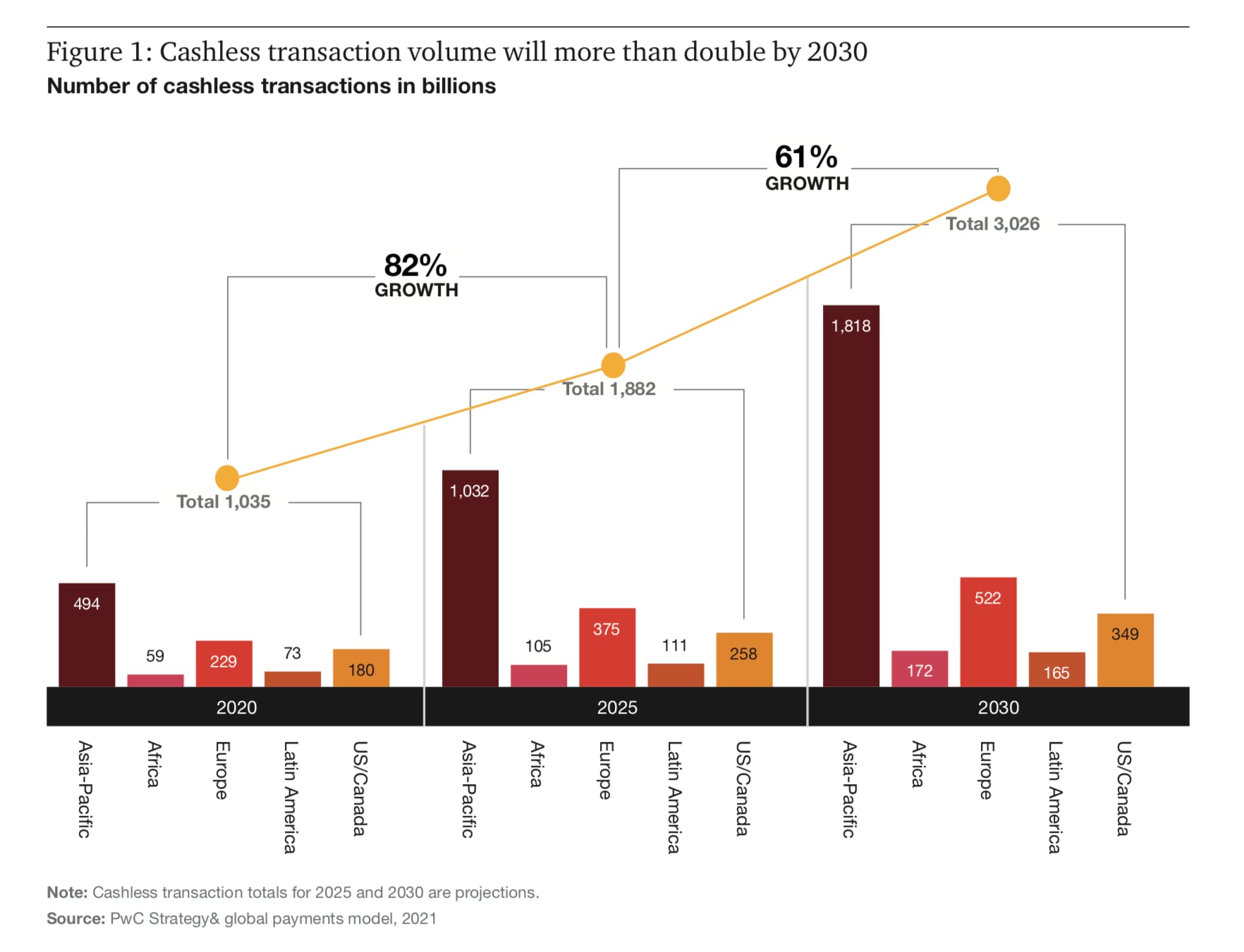

Even before COVID-19, the increasing use of texting, QR codes or tapping mobile phones were evidence of a steady shift to digital payments— a shift that might ultimately lead to a cashless global society. Global cashless payment volumes are set to increase by more than 80 percent from 2020 to 2025, from about 1tn transactions to almost 1.9tn, and to almost triple by 2030.1

Asia-Pacific will grow fastest, with cashless transaction volume growing by 109 percent until 2025 and then by 76 percent from 2025 to 2030, followed by Africa and Europe.

This means that by 2030 the number of cashless transactions will be about double to triple the current level, across regions.

Underneath the shift lies a larger, more profound change. Not only are traditional ways of paying for goods and services — including the humble paper check and analogue invoices — set for radical transformation, but the entire infrastructure of payments is being reshaped, with new business models emerging.

That reshaping involves two parallel trends: an evolution of the front- and back-end parts of the payment system (instant payments; bill payments and request to pay; and plastic cards and digital wallets); and a revolution involving huge structural changes to the payment mix and ecosystem (emergence of so-called “buy now, pay later” offerings; cryptocurrencies; and work underway on central bank digital currencies).

Six macro trends — driven by a combination of consumer preference, technology, regulation and M&A – will define how the next five years play out.

In 2014, the World Bank set a goal under its Universal Financial Access program that by 2020, adults who were not part of the formal financial system would be able to have access to a transaction account to store money and send and receive payments.2 That goal is still some way off from being achieved, but a growing number of initiatives are addressing it.

In developing countries, financial inclusion will continue to be driven by mobile devices and providing access to affordable, convenient payment mechanisms. By 2025, smartphone penetration is estimated to reach 80% globally, driven by uptake in emerging markets.3 Trust in these systems, particularly as central banks consider the feasibility of CBDCs, puts new emphasis on the role of supervisors to ensure data privacy and traceability for consumers and businesses.

CBDCs — digital tokens or electronic records that represent the virtual form of a nation’s currency — along with private sector cryptocurrencies are predicted to have the biggest disruptive impact over the next 20 years. The report found that financial services organisations surveyed in Europe, the Middle East and Africa with more than US$5bn in revenues cited “market uncertainty and potential disruption,” such as the introduction of CBDCs, within their top three concerns.

Scepticism within central banks about the potential of private sector cryptocurrencies to undermine the conduct of monetary policy may begin to shift, as some players have said they’re prepared to facilitate use of such digital assets.4

Digital wallets allow consumers to load and store payment methods and access funding sources, such as cards or accounts, on their mobile devices. These wallets will be increasingly pivotal as a payment ‘front end,’ as exemplified by Apple Pay, the relaunched Google Pay and the rise of WeChat Pay and Alipay in China.

The use of digital-wallet-based transactions grew globally by 7 percent in 2020, according to a report by FIS, which predicts that digital wallets will account for more than half of all e-commerce payments worldwide by 2024, as consumers shift from card-based to account- and QR code-based transactions.5

Looking ahead, as many as 86 percent of the 2025 & Beyond survey respondents agreed with the prediction that traditional payments providers will collaborate with fintechs and technology providers for innovation. 45 percent of respondents ‘strongly agreed’ that there will be increased investment in mobile technology beyond retail payments to support business-to-business (B2B) payments and the digitalisation of supply chains.

Behind-the-scenes payments processing — the ‘plumbing’ of payments — is also changing, as payment initiation changes from cards and traditional accounts to digital wallets and as regulators force the industry to strengthen, or build up, domestic infrastructure for payments.

As a result, international card networks and card processors, often US-domiciled, are facing pressure on their core business, and have started to reposition themselves to retain relevance. Outsourcing of cloud and platform infrastructure will become increasingly important, too. Eight out of ten financial services organisations surveyed for the report expected to have outsourced such infrastructure by 2025.

Processors and networks will also need to ensure relevance in the merchant services space, where payments are initiated.

Frustration with the traditional correspondent banking model, both cumbersome and costly in a world of instant, low-cost payments, has led to the intensification of non-bank providers. New players and solutions are competing with bank and card-based solutions at scale.

In the report, 42 percent of respondents surveyed felt strongly that there would be an acceleration of cross-border, cross-currency instant and B2B payments in the next five years. This is reinforced by the adoption of ISO 20022, a globally developed methodology for transmitting data which provides a consistent messaging standard for payments.

The pandemic’s effect in driving increased e-commerce provided an opening for fraudsters, with the average value of attempted fraudulent purchases rising by almost 70 percent in 2020, compared with the previous year.6

Open banking, combined with a set of new players and the shift towards payment initiation and digital wallets, is also opening new doors for all types of financial crime, such as the increased risk to consumers from authorised push payments (APP) scams across payment networks, globally. Payment providers that help merchants and their customers move money across borders might also enable sanctions evasion and money laundering.

Accelerated by the pandemic, the shift to a cashless society and the rising role of payments as more than simply an exchange of value for goods and services create a once-in-a-lifetime opportunity for the payments industry to lead in financial services. At the same time, by becoming a cornerstone of the global economy, payments can serve as a catalyst for economic growth, innovation and inclusion.

Organisations need to define what their role will be in this evolution. It is critical to understand what they need to do to stay relevant and how to improve the customer experience and contribute to a bigger societal purpose.

Download the full report for further insights from the first in our Payments 2025 & Beyond series.

References

{{item.text}}

{{item.text}}