{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

It’s been ten years since PwC launched the first Digital IQ Survey, as a way to gauge the digital acumen of organisations. In that time we’ve seen many changes, including the transition of digital from a term synonymous with IT, to a core mandate of the business of the future.

A decade ago, just 33% of our global respondents said their CEO was a champion for digital. Now, that figure is 68% – and even higher in Australia. Digital-driven change sits top-of-mind for the business leaders of today and transformation is now as much about business model and customer or employee experience as it is about the technology behind such changes.

Yet since we started asking executives to rate their own Digital IQ – that is, how well the value of digital technology is understood and weaved into the organisation – globally, Digital IQ has been slipping.

What we can see is that leaders have done something, but not enough, to stay abreast of the digital revolution. The pace of change is faster than our ability to actually respond, like a rate of inflation with which we cannot keep up.

The survey canvassed over 2,200 global executives (50 of them from Australia), to understand the approach to digital transformation in organisations across a range of industries. Here’s what the Australian results revealed:

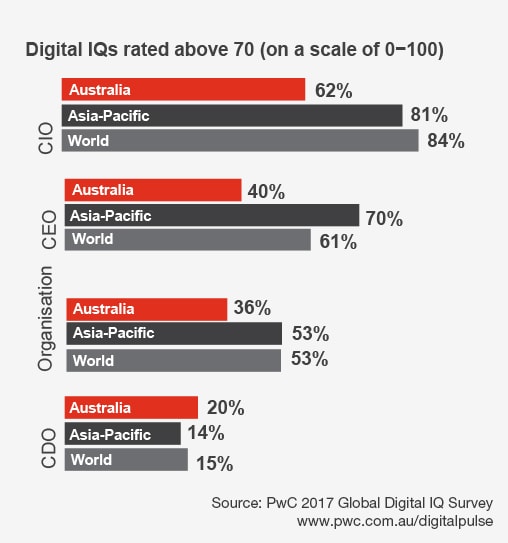

Each year, we ask participants to rate the Digital IQ of their organisation as a whole, as well as selected members of the C-suite.

Australian respondents had less confidence in executives than their Asia-Pacific or global counterparts did. This was true of all roles except the CDO.

A fifth of Australians ranked their CDO as having a high Digital IQ; globally, the figure was 15%. Australian firms are also slightly more likely (18%) than the rest of the world (6%) to employ a CDO.

The chief digital officer is not a homogenous role. A fairly new addition to the executive line-up, we’ve identified five different archetypes of CDO. This begs the question: we may have relatively more CDOs in Australia, but what type are we hiring? Are they technology focused? Or innovation or customer focused?

“Rate the Digital IQ of each of these leaders in your organisation in terms of how well they understand the value of digital technology and weave it into the parts of the business for which they are responsible.” World stats indicate answers from respondents outside of Australia and Asia-Pacific.

Globally and in Australia, CIOs are considered to be the most digitally savvy of all the C-suite.

Yet, in Australia only 10% of CIOs are involved in setting digital strategy, whereas globally, that responsibility falls almost equally between the CEO and CIO (48% and 44% respectively). Australian organisations almost always leave those decisions to the CEO – whose Digital IQ is rated much lower.

The statistics suggest that the Digital IQ of Australian leadership is lagging because it fails to seriously incorporate digital into the fabric of the business.

When asked ‘If you do not have a CDO, why not?’ most respondents said it was because the CIO or another executive fills the role. In Australia, however, almost a quarter said it was because digital isn’t a significant part of the strategy (only 3% of global respondents, and 2% of those outside Asia-Pacific, answered the same).

Globally and locally, CDOs are not given the mandate to drive critical digital activities: only 2% of businesses here say their CDO drives the corporate strategy.

Australians were much more likely to say ‘Our CEO is a champion for digital’. If this isn’t backed up by a roadmap to match, then being a champion of digital is, in some respects, irrelevant. The CEO is often focused on maintaining business-as-usual – so the fact that Australian companies leave high-level digital strategy largely in their hands, and not other digital executives, is a red flag.

In addition, results showed that nearly all Australian companies agreed that ‘digital technology investments are made primarily for competitive advantage’.

The takeaway here is that we’ve got a good story and the right level of sponsorship from the top – but the investments are more about the immediate returns of beating the competition, than around the more far-sighted goals of business model innovation.

When asked about the most important digital initiative that organisations will invest in in the next 12 months, ‘technology platform and integration’ was at number one, followed by ‘customer experience’ and ‘product/service/business model innovation’.

This rings alarm bells. The perfect starting point for any digital initiative is to rethink the service and reassess the product; every disruptor has a totally different business model to the business it’s disrupting. Business model innovation, therefore, should sit firmly in first place, customer experience is also important; technology should serve to support them both.

In addition, when asked what value is expected from digital technology investments, nearly three quarters of Australian respondents said that it was to grow revenue. Only 8% think their investments will enable better customer experiences. How can you grow revenue without creating better customer experiences? Surely that’s the statistic that should be 74%!

Furthermore, when asked how their organisations define digital, most executives answered ‘all technology-related activities’, followed by ‘digital is synonymous with IT’.

This tells us that Australian businesses place too much focus on technology, and not enough focus on strategy and experience. This is reflected by what we see on the ground – where ‘digital’ and ‘technology’ are still used interchangeably.

Both in Australia and globally, executives rate artificial intelligence (AI) and the internet of things (IoT) as the most disruptive technologies to their industry. Australians are also broadly investing the same amount as their global peers in different technologies.

While the internet of things and artificial intelligence are the investment priorities of today, funding for the IoT looks set to be downgraded in favour of significantly ramping up investment in robotics and augmented reality (AR).

Three years might even be overkill: these statistics are already supported by what we’re seeing on the ground with our mainstream Australian clients.

In fact, Australia seems to hold the internet of things in lower regard than our global counterparts. We don’t believe it will be as disruptive to industry or business model in coming years, nor do we consider it as important to cutting costs. Australian firms also reported their staff to be far less likely to have highly or quite developed skills in the IoT (22% compared to 41% globally).

Improving the customer experience is a key concern for Australian companies in our survey. They place a greater focus on the ways new technologies will affect human experiences (82%, vs. 70% globally) and they’re more likely to invest in customer experience initiatives (22% ranked it as top investment versus 11% of others).

However, while there is strong awareness of the value of customer experience – which is a critical dimension of Digital IQ – it has yet to be prioritised over technology investments.

Ten years can feel like a long time: it’s been enough to drive mobile, social and cloud into the mainstream, and set the stage for groundbreaking technologies such as virtual reality and blockchain. Yes, things are moving quickly.

However, what appears to be a steady reality across a decade of digital is that our inability to keep up with the pace of change is accompanied by a failure to embrace the era that we live in.

Organisations are heavily focused on technology and not fixated enough on the basics of brand, value proposition and advocacy. How does digital technology enable you to fix those challenges in today’s age, given that the connectivity between you and your customer is predominantly through technology means, as well as physical?

Unless that question is addressed, Digital IQ probably won’t be enhanced. If your value proposition is flawed, technology won’t fix it. It’s just going to highlight it more, and create more costs for your business.

How do you compare to the global Digital IQ results? Learn more about A decade of digital: Keeping pace with transformation here.

Note: Where comparisons have been made with ‘global’ statistics that figure includes Australia and Asia-Pacific. Comparisons titled ‘other’ or ‘rest of the world’ are between Australia and world figures excluding Asia-Pacific.

{{item.text}}

{{item.text}}