{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

Key takeaways

Before the concept of blockchain became famous in its own right, the talk of the town was Bitcoin. Blockchain, the technology on which Bitcoin is based, is now in the limelight itself, presenting a broader landscape of opportunity that goes well beyond digital currencies. The federal government even mentioned blockchain in its May budget, announcing a feasibility study for the technology’s deployment in the public and private sectors. Yet the majority of companies operating in the financial services industry are at this stage still grappling with where blockchain can fit into their broader strategy and what business problems it actually solves. In March this year, PwC released its global fintech report, Blurred Lines, which reported that around half of respondents – all working within the financial services industry – are either slightly or not at all familiar with blockchain.

This isn’t too surprising; as such a fundamentally new concept, blockchain still presents something of an enigma to many. However, it can basically be described like this: in the past, general ledgers and accounting records were stored in centralised databases. Now, imagine that database being encrypted and shared across a network where all the participants have a copy of that data. In order to create a record (or, rather, add a new block to the chain), a majority of the participants have to reach a consensus about that addition. This also means that once a record has been made to the database it can never be changed or corrupted. In this way, blockchain is also known as a ‘distributed ledger’.

Like many emerging technologies, blockchain is subject to hype and speculation. It’s important to understand we’re only very early in the journey of how to commercialise it and this year will be very much about pilot or proof-of-concept projects. Next year we expect to see the beginning of production deployments and the emergence of true commercialisation and value.

“Blockchain is a technology that is clearly disruptive, but what it will be, we don’t know,” said Dave Curran, CIO of Westpac bank recently. Indeed, 56% of PwC survey respondents recognise the importance of blockchain but around the same amount say they’re unsure or unlikely to respond to the trend.

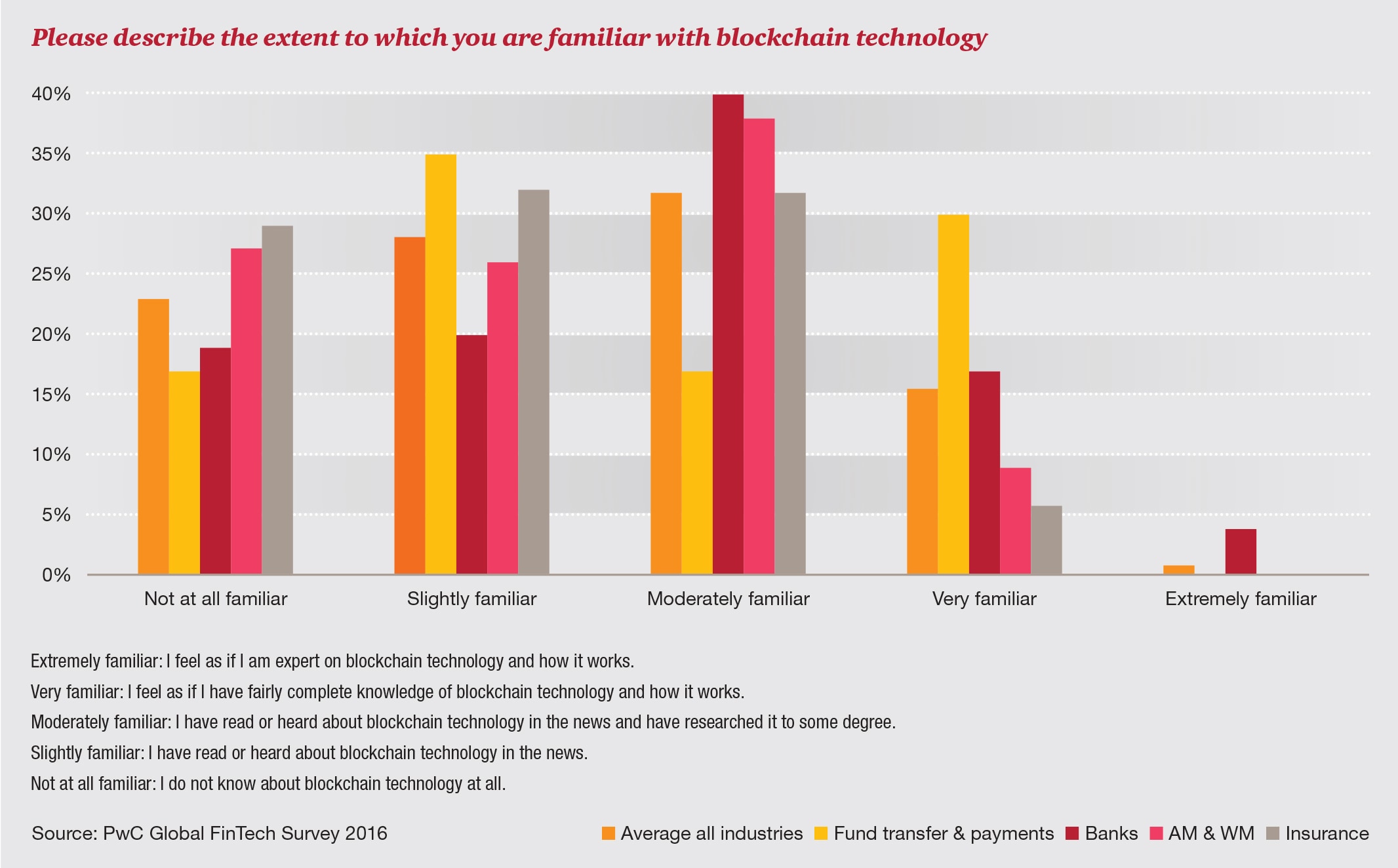

PwC’s 2016 Blurred Lines global fintech report revealed that very few of the financial services industry consider themselves experts on blockchain technology. (Click on image to enlarge)

The Blurred Lines report also revealed that very few respondents consider themselves to be experts on blockchain. It’s this lack of familiarity that may lead market participants to underestimate its potential impact on their activities. However, that level of understanding and familiarity varies across sectors.

Almost a third of fund transfer and payments companies consider themselves very familiar with blockchain – not surprising given the potential impact it’s likely to have on their business processes – whereas just 6% of insurers say the same.

Like all new technologies, it can take time for the dust to settle and for blockchain to be seen as a mature and robust technology. It also might not be a solution that works in every sector of the financial services industry.

Use cases that centre on increasing efficiency by removing the need for reconciliation between parties seem to be particularly attractive. For example, multi-party processes such as the settling of accounts in the stock market can be made more transparent and efficient if all the involved parties have access to the same information at the same time. This can reduce settlement times and decrease the need for later reconciliation.

Efficiency gains will come from the removal of slow, manual and exception steps in existing end-to-end processes driven by more streamlined and automated business logic. Risks will be better managed because blockchain data is written in real time to multiple parties. That means everyone gets a current view under a consensus model that results in greater confidence and trust in the data being recorded. These gains in transparency will also be very beneficial from an audit and regulatory point of view.

Blockchain technology will create structural shifts in the financial services industry and disrupt today’s profit pools. Changes in businesses processes as new entrants force their way into evolving blockchain-driven markets will benefit the owners of new, highly efficient blockchain-based platforms.

To highlight the competitive potential of blockchain in the financial services arena, data from PwC’s Global Blockchain Team has found in excess of 700 startups vying for supremacy in this emerging market. Of those, 25 are considered likely to emerge as leaders.

Many people imagine blockchain to be a solution in itself, but that is not the case. Blockchain is effectively a database, albeit a new style of one, however, it has the potential to be to financial services what TCP/IP is to the internet.

TCP/IP is a communications protocol over which data is exchanged between computers. It has a number of components, many of which we usually take for granted. For example, TCP/IP ensures that each piece of data that is transmitted is validated at the origin and destination. What makes TCP/IP useful is what we do with it.

The same applies to blockchain. While the protocol exists, we still need to develop applications for it, and in fact Bitcoin can be thought of as only the first application to sit on the public blockchain. So, the question for businesses should not be ‘How can I use blockchain?’ They would be better off asking: ‘What process am I doing today or am I planning to do tomorrow that can be made better by running it over the blockchain protocol?’

There are still some challenges to overcome before blockchain enjoys wide use:

As an emerging technology of significant potential, blockchain needs to be on the radar of the financial services industry. Here are some suggested action points:

For further advice on implementing blockchain, check out A strategist’s guide to blockchain in Strategy&’s strategy+business.

With thanks to Robert Allen, Payments & Blockchain Technology Consulting Leader, for contributing to this article.

{{item.text}}

{{item.text}}