Share this article

The turn of the calendar year presents a timely opportunity for employers to reflect on key areas of focus and resourcing, particularly in the context of controls and risk frameworks and governance.

PwC recently had the pleasure of hosting Australian Taxation Office (ATO) Deputy Commissioner for Superannuation & Employer Obligations, Ms Emma Rosenzweig, for the Payroll Leaders’ and Employment Taxes Forum. The Deputy Commissioner provided valuable insights into the ATO’s current aims and activities and in this article, we summarise key takeaways from the event.

Transition Plan: Single Touch Payroll - Phase 2

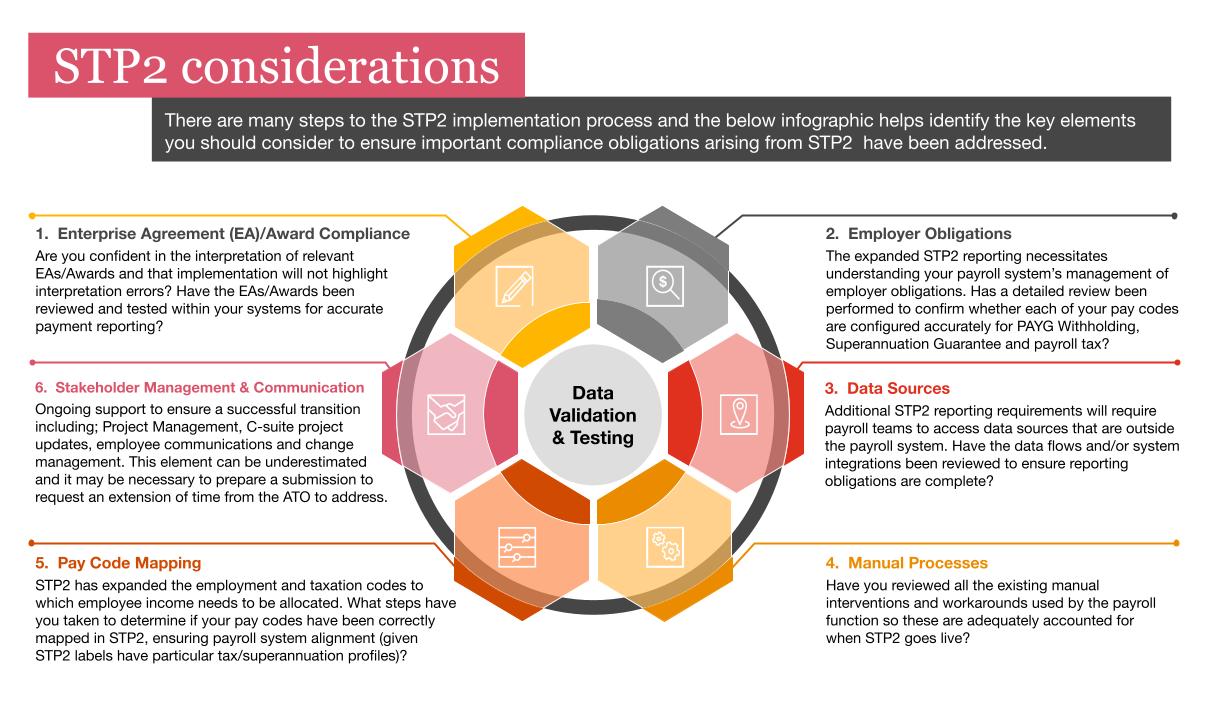

The Deputy Commissioner noted Single Touch Payroll Phase 2 (STP2) requires employers to provide more granular payroll information to the ATO which is shared with Services Australia to assist with administering the social security system in a more efficient, accurate and timely manner. As part of transition, the ATO recommended robust testing across three key areas:

- Undertake a payroll review and conduct payroll mapping to ensure you are meeting Fair Work requirements and Taxation and Superannuation obligations

- Review the pay code categorisations to STP2 labels

- Review access to non-payroll data

In our view, the areas noted by the ATO are pivotal to a successful transition. For reference, included below is PwC’s STP Readiness Wheel (steps 1-5 directly correspond to the ATO’s recommendations above).

Governance focus

The ATO urged employers to apply a governance “checks and balances” lens across payroll and employer obligations, whilst ensuring timely voluntary disclosure of non-compliance. As an example of avoidable errors, the ATO noted that its focus on PAYG had identified a significant number of PAYG discrepancies arising from employers remitting under incorrect ABNs or payment reference. The ATO conducted 675 reviews and recovered $470 million unpaid PAYG and general interest charge. In their latest reviews, the ATO identified inadequate payroll governance procedures and failures to undertake reconciliations and verification checks. It was also stressed that employers should not rely on third party reporting and be sure to review outsource payroll arrangements: “Ultimately it is you who has responsibility and accountability to meet your tax and super obligations on behalf of your employees”.

Compliance focus: Superannuation Guarantee (SG)

The ATO emphasised its commitment to a “preventative” and “proactive” SG compliance approach, including utilising STP2 filings. It was noted that, in response to the Australian National Audit Office Report, the ATO will review targets and publish its compliance performance. Given this regulator focus, we recommend employers develop ongoing testing of superannuation contributions against superable earnings, particularly those disclosed through STP2 reporting.

Evolving landscape: Contractors

With respect to contractors, the ATO noted that superannuation obligations exist where the arrangement in fact constitutes common law employment, or alternatively because of extended SG rules. In particular, the Deputy Commissioner noted that the recent High Court decisions had shifted the common law assessment, with additional case law imminent on the extended SG rules. If not already done, employers should review their contractor arrangements, documentation and substantiation, including a focus on both the common law assessment and the extended SG rules (noting again the potential impact from upcoming case law).

Car parking changes: Fringe Benefits Tax (FBT)

The ATO noted that TR2021/2 has expanded the FBT net to include penalty-rate chargers (e.g. shopping centres). Further, a ruling addendum was also cited as clarifying the meaning of ‘primary place of employment’ in light of recent case law. With respect to the expanded interpretation, employers should review all parking locations, particularly those within 1km of penalty-rate chargers that were historically excluded. Where potential FBT may result from the broadened test, an analysis should be undertaken to identify the lowest rate (e.g. unadvertised discounts) to ensure an accurate tax outcome.

Electric Vehicles (EVs): FBT

It was noted that the ATO will be releasing public guidance on EVs and FBT, currently aimed to be released post enactment of the Labor Government Electric Vehicle Exemption Bill. With numerous employers looking at fleet transitions to EVs as part of ESG, the proposed guidance will be important for the purpose of understanding and clarifying the ATO’s perspective regarding the tax treatment, in particular of tangential benefits such as in-home charging, charger cost/installation, battery replacements, etc. - we recommend employers ensure these are contemplated when designing their EV migration.

“New” ATO solution: super stapling

In December 2022, the ATO will provide a solution that payroll providers can implement to automate the request for a stapled fund (removing the need to separately use ATO Online Services). Further, from mid-2023, the interim bulk request process will be decommissioned; employers should consult with their payroll providers.

Interpretation of Ordinary Time Earnings (OTE): SG

In answering a specific query regarding the recent Finance Sector Union of Australia v Commonwealth Bank of Australia [2022] decision, which concerned the superability of leave loading payments, it was confirmed that the case is under ATO consideration and that, if the case is determined to be of significance, ATO commentary and product (e.g., SGR 2009/2) revision may follow. PwC recommends that employers monitor developments in this regard, given the potential impact of this case on the interpretation of not only the superability of leave loading, but the OTE base more generally.

If you would like to watch the presentation the on-demand video is available by clicking here.

Contact us