Share this article

In Australia, momentum is increasing towards climate action, net zero targets and greater sustainability of resources. But digging a little deeper exposes a less rosy picture in some sectors of the economy.

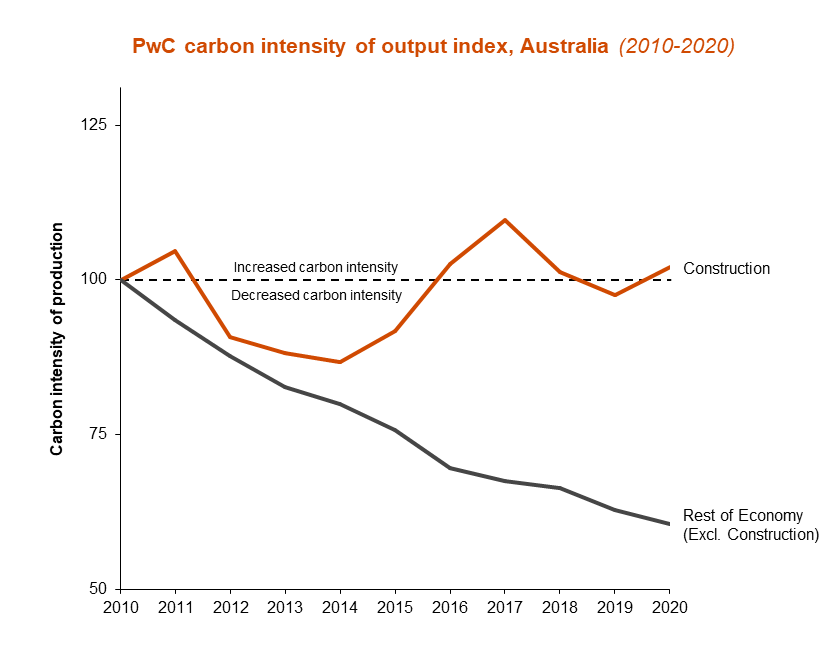

PwC modelling and data analysis1 across 19 major industry sectors reveals that the construction sector is progressively becoming even more carbon intensive, despite national decarbonisation and significant gains in the energy industry.

When we looked at the relationship between industry activity and emissions intensity across the whole economy, we found the construction sector isn’t decarbonising relative to its economic output when compared with the Australian economy. It’s a concerning finding, and perhaps for some a surprising one, given the amount of progress that’s been made in reducing operational emissions in the sector through energy efficiency initiatives. A significant component of the problem lies in embodied carbon – i.e. the carbon emissions generated in the manufacturing, transport, construction process and lifecycle of construction materials.

Since 2010, the construction sector's emissions relative to its economic contribution has increased, in contrast to almost all other industries. In addition, construction and demolition is also responsible for 38% of all waste (29 million tonnes per annum2). Materials such as steel and cement are highly emissions intensive and the sector is also significantly climate-exposed through its dependence on material extraction. Climate change is already having impacts on the availability of raw materials, which is causing instability in supply chains and fluctuations in pricing. Yet with spending on infrastructure projects increasing and the need for housing continuing to grow, demand for materials is escalating.

To halt this worsening problem, the sector will need to embrace alternative low-carbon materials. It must also find ways to use less new materials by optimising design and increasing material reuse and circularity. But it’s a notoriously difficult sector to abate. It takes significant will, time and money to change how we build and the materials we use.

While there have been various examples of innovation and progress in individual, novel construction projects, it will be a massive challenge to scale up and mainstream these new approaches sector-wide.

With challenge comes opportunity

Taking action to reduce embodied carbon in the construction sector is undoubtedly an intrinsic public good. It also makes good business sense. Building companies are starting to feel the pinch from the escalating costs of building materials and instability in supply chains. Assumptions that construction materials are abundant and readily available simply don’t match current realities, with materials increasingly scarce, costly and time-consuming to produce.

This situation presents an opportunity. Manufacturing low-carbon materials in Australia can create a more financially resilient construction industry and mitigate fluctuations in the availability and cost of raw materials. Taking up green materials in the construction industry supply chain makes good commercial sense and can mitigate climate risk exposure. Although recycled, low-carbon materials may lead to pressure on margins, that margin predictability and stability should improve with greater resilience in your supply chain. In an increasingly uncertain environment, limiting climate risk is a critical factor to future financial success.

There is also the chance to make the most of Australia’s significant comparative advantage in renewable energy to grow an export-oriented manufacturing industry geared for growth in a net-zero global economy.

In the short term, success will require support to overcome the ‘green premium’ by growing the demand for low-carbon materials, increasing scale (making more of a product is usually cheaper per unit of product), fostering innovation (improving and optimising production processes), and accounting for the cost of carbon.

Making change happen

To make rapid, meaningful change, every part of the construction industry needs to play a role, from designers, builders and developers through to investors, purchasers, government and regulators.

In particular, government has a range of very powerful levers at its disposal to encourage green materials demand and industry development. If government accelerates its intervention through purchasing mandates and increased procurement of green materials, the industry will grow, leading to greater competitiveness and preferencing of low-carbon materials.

Government can also support decarbonisation of the construction sector by risk-sharing on new technology, ultimately encouraging more supply of green commodities. Policy support is needed to stimulate early-stage technology development (such as through the Australian Renewable Energy Agency, funding for Cooperative Research Centres, and the Low Emissions Technology Statement) and to stimulate recycling and manufacturing.

Action on certification schemes and construction regulations and standards has significant potential to accelerate change. Options could include mandatory climate disclosure to attract international capital to the green construction commodity industry, and regulations that cap the embodied carbon per unit (km/sqm). Inclusion of embodied carbon intensity into national construction standards would create greater national consistency and enable Australia to embrace the export opportunity by demonstrating equivalence with other countries that have standards in place.

Greater action on embodied carbon will also require more awareness and education across the sector and the public. This could be facilitated through targeted information campaigns on the risks and performance of low-carbon alternatives, design guides, and rating tools or calculators for embodied carbon. For example, NABERS (the National Australian Built Environment Rating System) is developing a rating tool for embodied carbon to create a national baseline for performance.

It will take significant action from both government and the private sector to tackle the embodied carbon challenge in the construction sector – and change is needed now. Moving beyond resource exploitation and carbon intensity to a lower waste, greener built environment is the right path for sustainable growth.

About the authors

Dr Lucas Carmody is an Executive Director in PwC's Global Centre for Nature Positive Business. Lucas is an economist specialising in the implications of the transition towards a clean and green economy.

1. PwC’s Geospatial Economic Model (GEM) Emissions Module allows us to combine industry-level economic and CO2 data at the level of local economies across Australia. GEM tracks emissions and industry economic output over the past 15 years for over 2,214 locations across Australia in a manner consistent and reconcilable with methods used by the ABS, DISER and DAWE.

2. https://www.dcceew.gov.au/sites/default/files/documents/national-waste-report-2022.pdf