{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

Consumer expectations are shifting as inflation, supply chain obstacles, ESG awareness and a possible recession affect availability, competition and values.

Advances in virtual reality and the oncoming metaverse are changing the meaning of ‘omnichannel’.

Recent waves of disruption are likely to continue shaping consumer behaviour, even as new waves break.

Still seeing the all-pervasive ‘customers may experience delays’ pop-ups on your favourite online shopping sites? Decreased opening hours signs in local shop windows?

These are messages consumers got used to during the early days of the COVID-19 pandemic as retailers and manufacturers went into self-preservation mode – simplifying supply chains, streamlining product lines and cutting back on customer service. It was a reasonable response to the uncertainty of the crisis, and many customers, struggling with their own COVID-borne life upheavals, understood and accepted that things weren’t operating as usual.

Two years later, with disruptions ranging from the pandemic, to war, inflation, supply chain problems, energy crises and worker shortages, PwC’s latest Global Consumer Insights Pulse Survey finds customers are beginning to lose patience as companies hesitate to fully re-engage.

The vast majority of global respondents to the survey, over 75%, plan to sustain or increase their current levels of spending in the next six months across most categories. Although the survey did not focus on inflation, it’s clear that consumers are aware of its effect, particularly when it comes to groceries. Around half of those surveyed, both globally and in Australia, said they expect to spend more on groceries in the next six months. Non-essentials such as fashion, health and beauty and consumer electronics are on the ‘spend less’ list – something to watch if inflation persists.

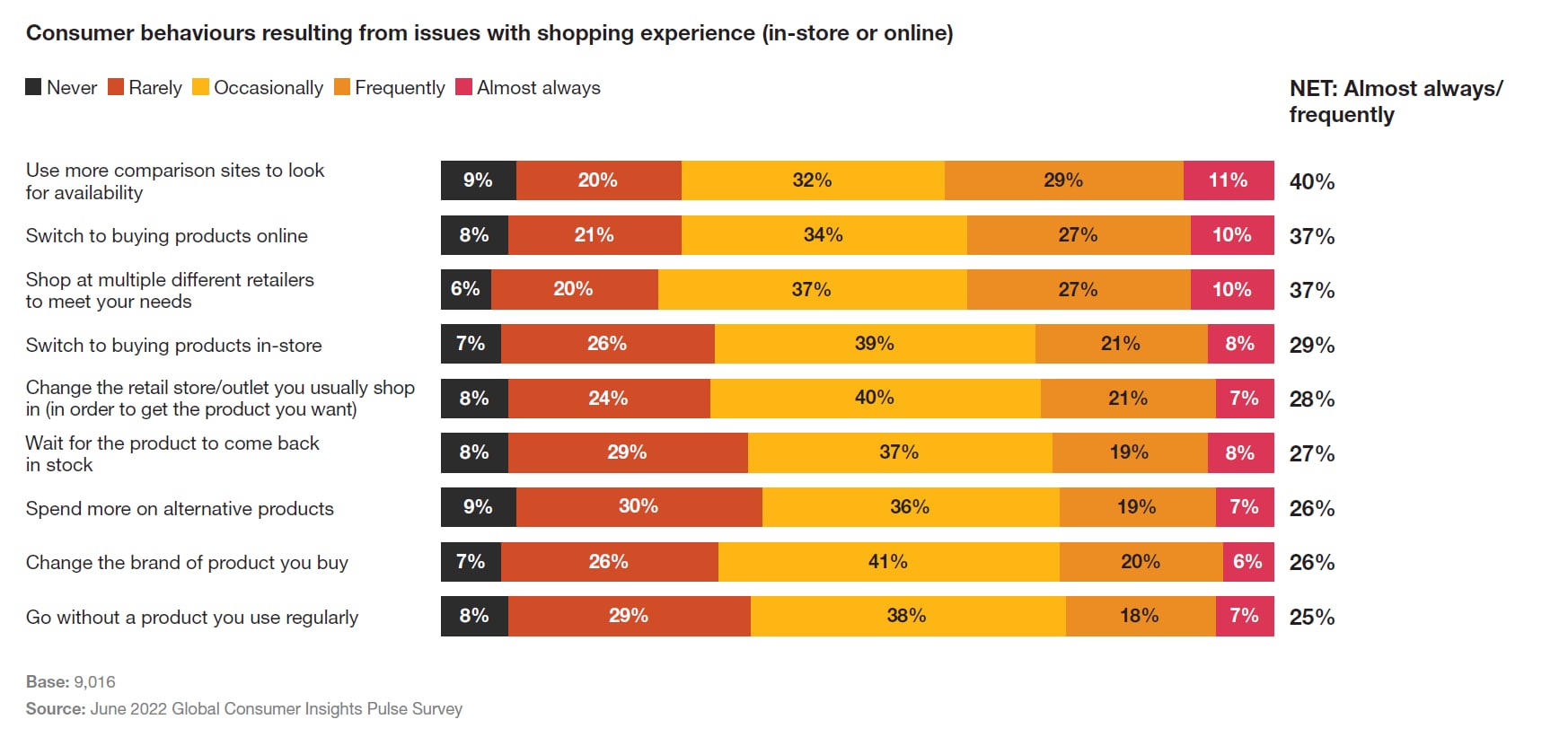

Supply chain obstacles are continuing to limit consumer choice and making it more likely for them to comparison-shop across retailers and channels. One in four global respondents said they were willing to pay more for what they wanted (in Australia, that rose to 1 in 3), but in both cases, just as many were willing to wait or go without. Additionally, shopping behaviour in-store has changed, with consumers experiencing longer queues and unavailability of products. When shopping online, more than 40 percent of global respondents say they are being impacted by longer delivery times and out of stock products (ranked in the top three). In Australia, the situation is reportedly worse, with 44 percent reporting longer delivery times, and over half saying products being out of stock is impacting their purchasing. Unsurprising, therefore, is the finding that Australian consumers are the most likely to report being affected by supply chain barriers.

Where and how products are made matters. Globally, and in Australia, 8 out of 10 respondents say they have some willingness to pay more for products produced locally or domestically. Most of these want to support their local economies, and around a third to support their country (global, 35 percent; Australia, 28 percent). ESG factors are also continuing to affect shopping behaviours, with millennials and Gen Z significantly more likely to keep them in mind when purchasing. All ESG factors – governance, social and environmental – seem to affect trust and advocacy, with around half of those surveyed saying it affects their trust in a company or brand, and the likelihood they will recommend it to others. Paying a fair share of taxes is a major influencing factor for 36 percent of global consumers and 39 percent of Australian consumers, as is admitting past mistakes (global 41 percent ; Australia, 46 percent).

As the online and physical worlds have merged, most retailers think they understand what omnichannel means, but virtual reality and the metaverse are changing the equation.

In the face of disruption, the importance of omnichannel has grown as customers use comparison sites to determine product availability and shop across multiple retailers to meet their needs. A whopping 81 percent of global respondents said they have shopped across at least three or four channels over the past six months, with more than half shopping daily or weekly.

Although some consumers are going back to in-store shopping, unmet delivery and quality expectations mean that neither online or physical has the advantage. Consumers are just as likely to switch between the two in either direction if it means they can get the product they want.

The metaverse is still an emerging channel, but consumer products companies and retailers alike may need to consider it as part of their omnichannel presence. Globally, one in three respondents report using a virtual reality channel in the last six months, and many of those for a retail experience. One-third of global VR users had joined a virtual world to experience a retail environment, the same number as those reporting purchasing digital products after testing or browsing stores in VR. Two in ten used VR to purchase luxury goods.

In Australia, respondents did not report significant VR use – at the moment it is most popular among respondents in China, India and Qatar, and relatively less popular for those in Australia, Ireland and Japan. As is the case with many new technologies, consumers in China are early adopters. VR was also popular among Generation Z and young millennials, as well as those of any age working in a hybrid model. Forty-five percent of global respondents who have used VR expect to increase their VR spending over the next six months in multiple categories.

Where do retailers need to adapt going forward? Omnichannel is an imperative thanks to the problems associated with the pandemic and its economic effects – VR should be added to the equation, quickly.

ESG, especially the social and governance, will grow as a disruptive force and as a driver of value with investors, regulators and governments all getting in on the action – and as consumers pay more attention to ethical standards and corporate values. Standards and regulations will change how consumer products companies and retailers do business, how products reach consumers and which products are available. Counter to this, if inflation continues to raise prices, consumer commitment to ESG values may waiver.

Finally, with recent volatility, economic contraction may be coming. A recession in major markets will inevitably affect consumer behaviour – and indeed, could alleviate the pressures on supply chains with a decrease in demand.

For more insights from the Global Consumer Insights Pulse Survey, visit the global landing page where you can compare and contrast country/territory responses.

Donna Watt

Partner, PwC Australia

{{item.text}}

{{item.text}}