{{item.videoDuration}}

{{item.title}}

{{item.videoDuration}}

Key takeaways

Trust. For such a small word, it certainly has a lot riding on it.

We place our trust in the people we know, the institutions who have earned or been bestowed it in law, the systems that allow anarchy to be kept at bay. Without trust, society doesn’t operate.

Clearly, trust is important.

Relationships, whether intimate or transactional, require that the person or entity being interacted with is trustworthy. That is, they are who they say they are, and their actions will lead to particular reactions.

But how do people know if a person or business is trustworthy? Particularly in a digital landscape, where face-to-face behavioural cues are often missing?

As it turns out, whether online or offline, mechanisms in which humans judge trust – consistency of behaviour, language, social cues and narratives over time – work online as they do offline. In fact, given the way in which digital lives are coded in data, it could be argued that they’re even more accessible.

Online, a company’s reputation, its behaviour and trustworthiness, is forever recorded and thus remembered. Good actions and ethics observed by consumers can be broadcast throughout the online world. But so can the bad ones.

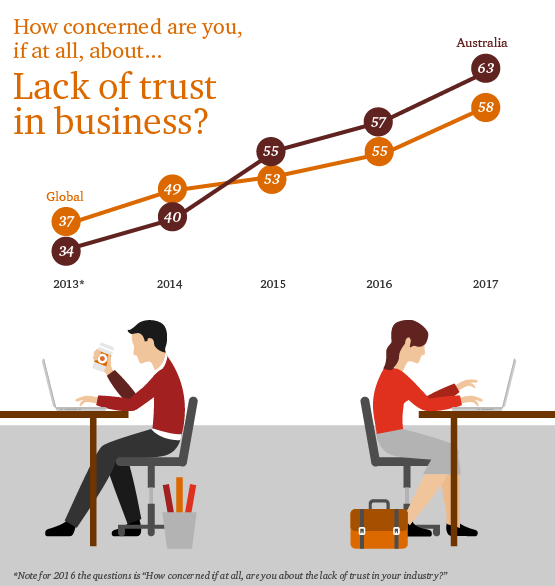

According to PwC’s 20th CEO Survey, business leaders are worried about trust. Significantly so. Consider that just 15 years ago only 12% thought that public trust in their companies had gone down and the majority (71%) weren’t at all worried that their corporate behaviour could have an effect on how people saw them.

Today, 69% of CEOs think that it’s harder to gain and keep trust due to the digital world we live in, where data can be breached and ethical lapses are public. More than half worry that a lack of trust in their organisation will harm their growth. In Australia, that number’s even higher, encompassing nearly two-thirds of leaders.

Source: PwC’s 20th CEO Survey

Unlike the CEOs of 2002, today’s post-financial crisis executives have a lot more to worry about with the entrenchment of the internet in business life and its associated risks. Concerns include data and privacy breaches, the rise of social media (87% of CEOs believe social media could have a negative impact on the level of stakeholder trust in their industry over the next five years) and the implementation of risk and governance frameworks around emerging technology, such as artificial intelligence.

Source: PwC’s 20th CEO Survey

“The breakdown in public trust,” says the CEO Survey, “now poses a potent risk to political, economic and social systems the world over. Every decision and action that business leaders take – whether it involves customers, employees, suppliers, partners, shareholders or the wider community – has a bearing on trust. In an increasingly transparent world companies need a clear moral compass. Stakeholders are keenly interested, not just in what businesses do but also in how and why they do it.”

The behaviour and ethics of a company’s leadership and staff has an effect on its trustworthiness. To 2017 ears, this seems obvious but in a pre-internet world, the chance of bad behaviour being discovered – let alone being broadcast to the world – was a lot slimmer.

Rachel Botsman, global expert on trust and collaboration, believes that reputation could become the currency of a new economy. Looking at the rise of collaborative consumption and the sharing economy, she cites the example of Airbnb, where it is the reputational score – itself driven by the human-touch of a host in making a stay comfortable – that is increasing trust between strangers.

Botsman argues that online trust has gone through three stages¹. From “trusting people online to share information, to trusting to handing over our credit card information, and now we’re entering the third trust-wave: connecting trustworthy strangers to create all kinds of people-powered marketplaces.”

If reputation is a device to allow strangers to judge the trustworthiness of each other, then it can be summed up as “the measurement of how much a community trusts you.” And as CEOs and businesses have found, reputation is incredibly important for trust.

According to Botsman, we could be at the beginning of a new ‘reputation economy’. If a person were able to own their behaviourally-based reputational score on one platform and associate that with their identity elsewhere, a new currency with which to trust would be born.

Warren Buffett, billionaire financier, sagely said, “It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you’ll do things differently.” For businesses in the reputation economy, shaping a good one and maintaining it in the face of customer scrutiny is harder than it used to be.

Consumer expectations around their retail experiences are high, and are continually becoming more sophisticated. To win the hearts of consumers, businesses must actively work on reputation management. Much like trust between individuals, this will also be judged on the consistency of a business’ brand over time.

This means a commitment to conformity of messaging and ethos, quality products, personalisation and flawless omnichannel communication. Organisations must understand their customers and use that information to deliver even better services. Moreover, companies need to be transparent in their dealings in order for consumers to be able to evaluate that behaviour.

Of course even when businesses do everything right with regards to experience, they can still be undone by the nature of digital. When data is connected, it can be accessed. Nothing will damage reputation quicker than a data or privacy breach (except perhaps, the mishandling of it).

Blockchain provides a potential solution to transactional trust on the internet². By decentralising transactional data via a distributed ledger, not only will data be transparently verified by the network, it will also be immutable, as tampering with it becomes near impossible without a) everyone else seeing it happen and b) the computing power required to change its instance on every computer the ledger is on.

While most famous for cryptocurrencies like Bitcoin, blockchain can be used for all sorts of data and, particularly in retail, all kinds of uses. While secure consumer payments and credit card information are the obvious usage cases for blockchain, so could it be used in proving the quality and pedigree of products³, shipping and postal efficiencies and in transferring warranties4.

While still early days for blockchain implementation, its potential for creating an internet of trust is high.

As the ways we evaluate trust and reputation change, it would be easy to think that business faces insurmountable challenges.

Yet, when asked in the CEO Survey, 64% said they thought the way they manage data will be a differentiating factor in the future. There is opportunity, therefore, in “prioritising the human experience in an increasingly virtual world.”5

Earning a consumer’s trust, the report found, is the single biggest enabler of success.

By focusing on being trustworthy in a digital age – be that in the interactions had with consumers or the technology and governance used behind the scenes, organisations will be well placed to earn and keep their reputation – and their customers.

References

{{item.text}}

{{item.text}}